Buried under a mountain of student loan debt with no end in sight? Looking for a way to finally achieve some financial freedom? Well, you’re in luck! In this ultimate […]

HOT RIGHT NOW

Comprehensive Guide to Student Loan Forgiveness Under the Biden Administration

“By a vote of 6-3, the Supreme Court justices ruled that the Biden administration overstepped its authority in 2022 when it announced that it would cancel up to $400 billion […]

Student Loan Forgiveness for Military Spouses

Many people have wanted student loan forgiveness for military spouses to become a reality for a long time. Some have wished for a disabled veterans spouse student loan forgiveness. All […]

RECENT

Buried under a mountain of student loan debt with no end in sight? Looking for a way to finally achieve some financial freedom? Well, you’re in luck! In this ultimate […]

Student loan consolidation is a popular option for borrowers looking to simplify their repayment process. However, there has been some confusion surrounding this financial strategy and its impact on credit […]

Are you struggling to keep up with your student loan payments? Wondering if there’s a way to ease that struggle? You’re not alone. Millions of students deal with the same […]

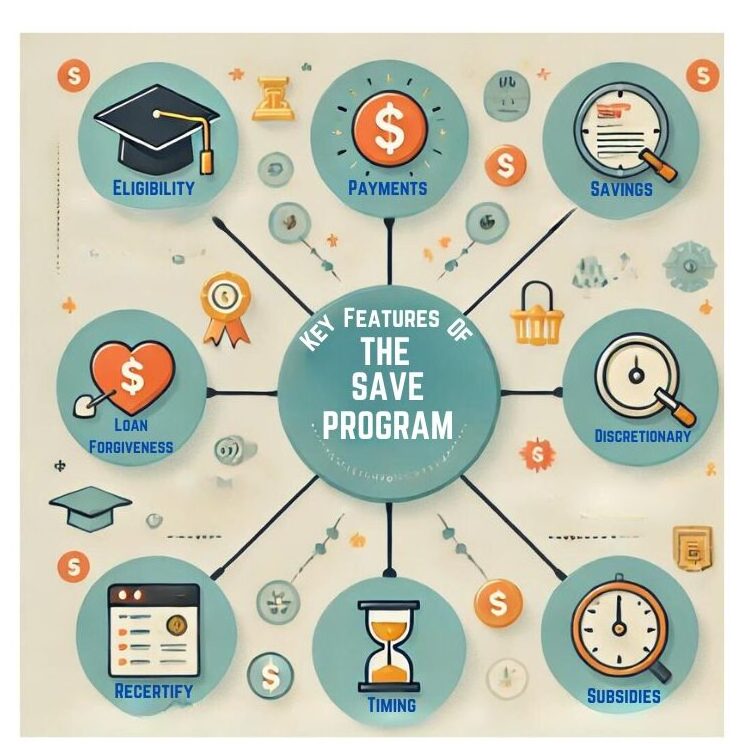

Understanding the Saving on a Valuable Education (SAVE) Repayment Plan: A Comparative Analysis The Saving on a Valuable Education (SAVE) Repayment Plan is a relatively recent addition to the suite […]

Debt Clock Current US Debt Clock

Are you drowning in student loan debt? Are you juggling multiple monthly payments and struggling to keep up? It’s time to take control of your financial future and simplify your […]

Understanding how to calculate your discretionary income is super important if you have student loans. It helps you figure out how much you might need to pay each month. Let’s […]

“By a vote of 6-3, the Supreme Court justices ruled that the Biden administration overstepped its authority in 2022 when it announced that it would cancel up to $400 billion […]

Navigating student loan repayment can feel like a daunting task, especially when your monthly payments strain your budget. That’s where the Income Based Repayment Plan (IBR) comes in. Designed to […]

Refinancing your student loans can be a smart financial move, potentially saving you thousands of dollars over the life of your loans. But what exactly does refinancing entail, and how […]

Feeling overwhelmed by your student loan payments? Don’t worry, there are several ways to make them more manageable. Here’s a guide to help you lower those monthly payments: 1. Income-Driven […]

What’s going on with Coronavirus & student loans? The Coronavirus pandemic has forced many businesses, including schools and universities, to operate differently than they used to. Some schools have closed, […]

The cost of a college education has risen dramatically in recent years. According to U.S. News & World Report, the average cost of tuition and fees for the 2019–2020 school […]

If you’ve just graduated, it’s time to face the music on your student loans. Your grace period will be over in a matter of months, and average student loans now […]

Many Americans struggle to pay their student loans. In fact, 10.8% of student loan borrowers are delinquent or in default on payments – that’s 5.5 million people. On average, 3,000 […]

It has often been said that “modern problems require modern solutions,” and the current $1.56 trillion dollar student debt crisis is indeed a modern problem. As the average student of […]

If you left college with a lot of student loans, and have started to struggle keeping up with payments along with daily expenses, you may be wondering if you can […]

Are you considering doing a student loan consolidation? If so, you’re in the right place. We’ll give you the lowdown on consolidation, when it’s a good idea and even show […]

Student loan debt has skyrocketed up to $1.56 trillion in 2020, with a total of 45 million borrowers across the United States. That makes federal student loan debt the second […]

Are you wondering what happens to your student loans when you drop out? You’re not alone. Let’s take a look at a few statistics. Just 56% of people who enter […]

What’s the difference between subsidized vs. unsubsidized student loans? When it comes time to pay for college, most Americans will seek out financial assistance. Whether this is in the form […]

Joe Biden: Policies on Student Loans & What It Means For You If Joe Biden does indeed emerge from the pending litigation and recounts of the current presidential election as […]

Many people have wanted student loan forgiveness for military spouses to become a reality for a long time. Some have wished for a disabled veterans spouse student loan forgiveness. All […]

Are you a student who has taken out loans to fund your education? If so, you may be wondering how those loans could impact your tax refund. In this comprehensive […]

If you’re looking for a way to have some of your Federal student loan debt forgiven, you may want to look into Public Service Loan Forgiveness (PSLF). In order to […]