Student Loans Are Worth Every Penny

We have published several articles about how the class of 2014 holds the title of the “most indebted class in history”, the average 2014 college student graduated with about $33,000 in student loan debt, definitely an all-time high. That amount is over 12% higher than the average for 2012 graduates, which has led a lot of experts and media people to believe that the student loan debt is a gigantic tragedy, it’s a fatal crisis, that is weighing down the U.S. economy, affecting the housing market, that basically it’s a “bubble” about to burst.

Whether or not the ridiculously high tuition costs and the resulting indebtedness that comes with it continue to climb at these absurd rates is anyone’s guess at this point.

The somewhat uncomplicated and easy student loan access creates an enormous pool of applicants every year trying to achieve their dreams of a college degree. These applicants come from all backgrounds and they all have different economic and financial needs, but since Federal Student Loans are guaranteed and backed by the federal government, this gives colleges and universities little to no incentives at all to stop the tuition hikes.

In spite of so many articles out there these days making you question if college is really worth it, and a lot of people deciding not to pursue their dreams of a college degree, well…it still somehow appears that college, and those student loans, are definitely worth the cost.

Here are a few reasons why borrowing to finance your education is well worth it, and some situations when it’s not.

If you choose the right career path, you’ll make your money back and then some

According to a recent study by Georgetown University, the average college graduate can expect to earn $2.3 million over their lifetime, and this jumps to $2.7 million with a master’s degree. With just a high school diploma, lifetime earning expectancy plummets to just $1.3 million. All of a sudden, being $30,000 in debt doesn’t seem like such a bad deal.

Ok, we don’t know exactly how many of those college graduates actually earn that amount of money, but the point is that, the more education you have, the more money you’re expected to make in your lifetime.

The median income for young adults (ages 25-34) is just $30,000 with a high school diploma, $46,900 with a bachelor’s degree, and $59,600 with a master’s or higher, according to the national center for educational statistics.

If you have the average student loan debt of $33,000, you can expect monthly payments of about $380 under the standard 10-year repayment plan, or $4,560 per year. So, the difference in salary more than makes up for the cost to pay off your debt. And bear in mind there are extended and income-based repayment plans which could make your actual payments much lower. The point is that you’re much better off borrowing and going to school than going right into the workforce after high school.

And, some majors have much higher salaries, making the loans well worth the cost. To name a few, accounting majors average a starting salary of nearly $55,000, computer engineering majors $58,000, and the average electrical engineering major starts at more than $60,000.

Alright, but what if I get a crappy low-paying job?

Sure, piling up a ton of student loan debt for a college degree may be worth it for engineers and accountants, but what about for students who aspire to careers with more modest salaries? What if I want to become an artist? or a teacher?

Well, first you must be aware that you will never be rich if you decide to become a teacher, but there are a handful of federal programs in place to make student loans way more affordable for those with low incomes. For instance, the recently expanded “Pay As You Earn” plan limits your student loan payments to just 10% of your discretionary income, and forgives any remaining loan balance after 20 years.

And, if you work in a public service career, such as teaching in a public school, law enforcement, social work, or many other non-profit careers, you could take advantage of the Public Service Loan Forgiveness option that takes care of the rest of your loan balance after just 10 years. For teachers, the deal is even sweeter, with an opportunity to have some of the loans forgiven after five years at certain public schools.

So, if getting a master’s degree to qualify for your dream job will put you $70,000 in debt when the job only pays $35,000, don’t worry. The actual amount you end up repaying should be much less than you borrowed.

The job security is nice, right?

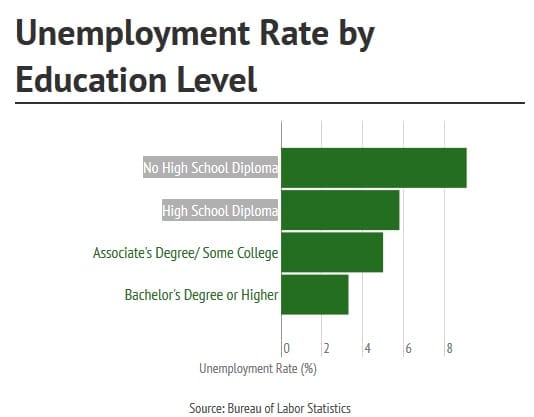

While the unemployment rate for very recent graduates is a little high (about 8.5%), once you land that first job, your employment outlook is much brighter with a degree.

The unemployment rate for all college graduates over 25 is just 3.3%, much less than the national rate of 6.1%. As you can see, the more educated you are, the better the unemployment picture is looking.

So What Does This All Mean To You?

Whenever you see a news headline about the “Student debt crisis” or the “tuition bubble”, take it with a grain of salt.

Tuition is much higher than it used to be, but a college education is well worth what it costs to get it. And, for those who end up earning less money or have trouble finding jobs, there are several ways to lessen the burden of student loan debt.

The takeaway here is that no matter what you read, don’t let the thought of taking out student loans prevent you from pursuing a college education.

Leave a Reply