Move over flex hours, foosball tables and free snacks! Student Loan Debt Employee Benefits Are Making Their Debut…

There’s hot new employee benefit making waves in the business world. An increasing amount of employers are offering student loan repayment as part of their benefits packages. This trend is aimed at recruiting and retaining young employees and is more practical than some of the perks previously used to entice potential employees.

Education debt has soared in recent years, nearly tripling since the early 1990’s and reaching an average of $35,000 in 2015. With the weight of this debt burden heavy on their shoulders, Millennials’ focus is not on retirement – it’s how to free themselves from the burden of their student loan debt.

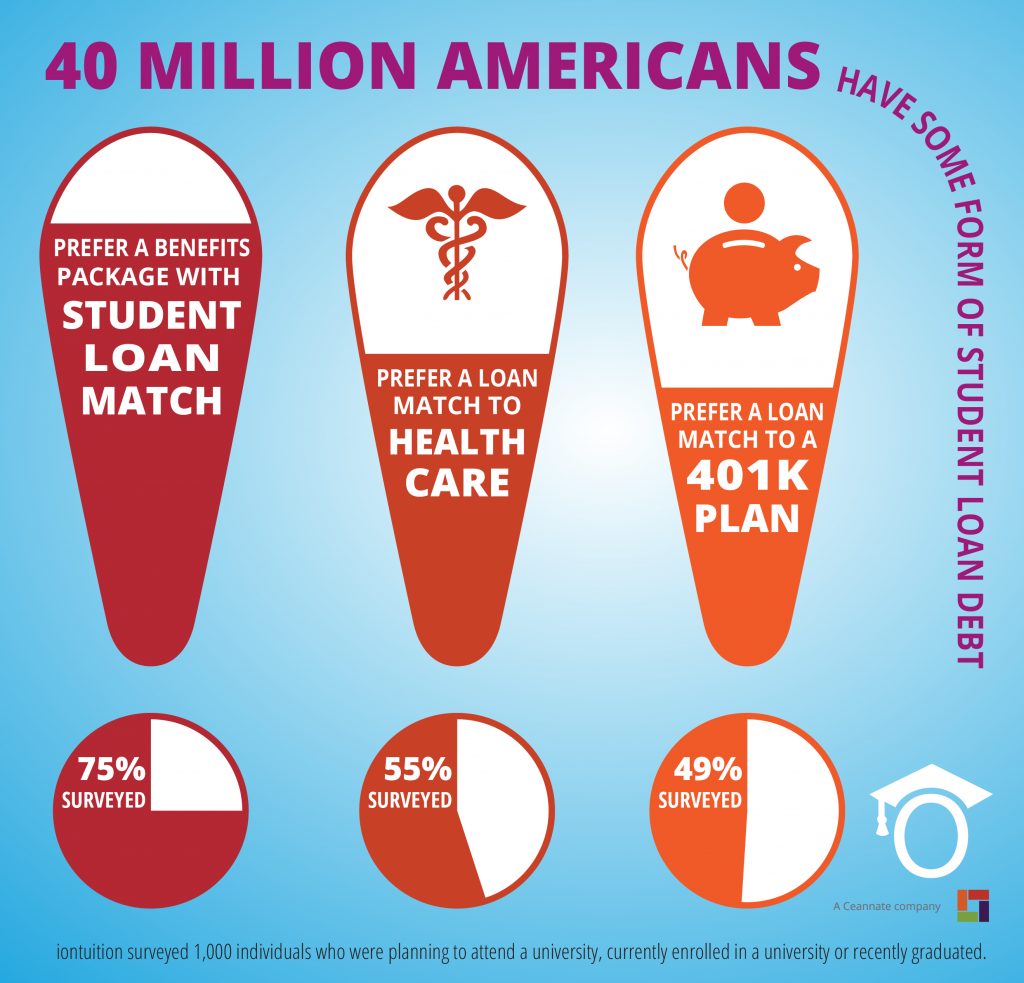

In fact, 55% of student loan holders said they would choose to divert health benefit contributions from their employer toward paying off their debt. Additionally, 49% said they would rather have student loan payment contributions than a 401k plan.

Although this is an exciting new benefit some employers are offering, a survey conducted by the Society for Human Resources Management reports only 3% of companies currently offer a student loan debt benefit. However, that number is expected to grow.

Especially since graduating from college with student debt is increasingly becoming the norm, not the exception.

Here are some additional details about this new trend that is sure to draw interest from the young workforce:

{How does it work?}

There is no standard set of rules or system in place yet, but generally the employer will agree to pay or reimburse a specific amount toward an employee’s student loans. The employee will still make their own payments while the employer’s benefit is sent directly to the loan provider by a third-party vendor and applied to the principal, reducing the overall size and length of the loan.

{How much will I save?}

Some perks look great on paper but, in reality, do little for employees. But student loan assistance isn’t just a buzzword employers use to reel in fresh talent; it has a true impact on employees’ financial well-being.

The value of this benefit is not only the amount that your employer contributes, but also the potential savings from reduced interest payments. Therefore the amount of those savings will depend on how much student loan debt you have.

{What are the advantages?}

What might be surprising to know is that, beyond recruiting, a company doesn’t have a lot of incentive to offer student loan debt employee benefits to you…yet. That’s because when companies help out with student loans, that assistance receives different tax treatment than the 401(k) benefit.

Employer 401(k) contributions are generally tax-deductible for the company and tax-deferred for the employee (meaning employees don’t pay taxes on that amount until they take the money out at retirement). In the case of student loan assistance, not only is the employer’s contribution not tax-deductible for the company, it’s actually taxed as income for the employee. This makes it less attractive for companies to offer a student loan benefit—and less beneficial for their workforce when they do so at this time.

Fortunately, a recently proposed student loan bill could change that.

{A promising future}

The “Employer Participation in Student Loan Assistance Act” was recently introduced in both the House and Senate with bipartisan co-sponsorship. If the bill passes, it would bring the tax treatment of employer student loan contributions in line with the 401(k). This would make it more compelling for employers to offer a student loan benefit.

If you have student debt, you’re probably already on-board with the idea of getting loan assistance from your employer.

But here are just a few of the great things that could happen if this bill passes:

- More employers would be likely to assist employees with student loans, since they would have a tax incentive to do so.

- Assistance from your employer would make more of an impact on your student debt, since you won’t be taxed on the contributions.

- As employees save money on student loans, they’d have more cash flow available to contribute to a retirement plan, buy a home, etc. This is not only good for the employee, but also great for the economy at large.

- The student loan default rate and delinquencies in the federal student loan program would go down.

{But What About Right Now??}

All of this sounds great, but if you need assistance with your loan right now it doesn’t do you much good. If you want to discover other avenues of student loan relief that you can take RIGHT NOW, without waiting for your employer to catch up with the trend, contact us today to explore your options at 877-433-7501.

If a student loan contribution was offered by a potential employer as a part of their benefits package would it entice you to take the job? Why or why not?

Leave a Reply