Did you ever think your dreaded monthly student loan payment could actually save you money? No? Well, we have some great news for you: It can—on your taxes.

Now that January has arrived, many people are receiving their annual income statements and W2s and preparing to file their 2015 income taxes. Another important document to watch for, if you have a student loan you are making payments on, is a 1098-E.

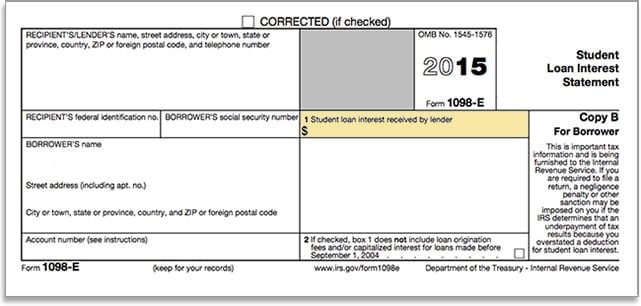

Here’s a sample of what it should look like:

The 1098-E is a document provide by your student loan servicer. It is a statement that will detail any interest you’ve paid on your student loan throughout the previous tax year. That’s good news for you, because just like interest paid on a mortgage, student loan interest can be tax deductible.

If you have more than one loan servicer, like a federal loan and a private loan, be sure to get statements from each servicer, so you will have a total of the entire interest amount that you paid during the tax year. Many servicers also provide the options to download documents from the website. Check with your individual servicer for details.

The student loan interest deduction can reduce the amount of income on which you are required to pay income taxes. Here are some important things to understand about the student loan interest deduction:

- You can deduct up to a maximum of $2,500 in student loan interest paid in the year.

- Your modified adjusted gross income cannot be more than $80,000 (or $160,000 for married couples filing jointly)

- You can only deduct the interest on loans from a qualifying source. Loans from friends and family are not eligible.

Other factors, along with your individual tax situation will determine if the student loan interest deduction makes sense for you. Be sure to speak to your tax professional.

Are you paying a lot of interest and high student loan bills? US Student Loan Center can help. Contact us today at 877-433-7501 to find out how we can help you with those high student loan payments.

Leave a Reply